{kind=link}

Resources Our platform

How to own your future on the premium open internet

Recruiting fraud is a growing issue for many companies.

The Trade Desk takes this issue seriously and is taking steps to address it.

Retail Media

A new analysis uncovers how shoppers navigate today’s purchase journey and the role media, messaging, and value play in driving decisions along the way. Plus, explore when and where media makes the biggest impact across 6 core CPC categories including food, beverage, and household supplies.

Share:

As tariffs threaten to drive up prices and slow down the economy, U.S. consumers are getting more selective about how they spend. Seventy-five percent of Americans say they’re more cautious with their finances than they used to be, and 58% report cutting costs by buying private-label products,1 which are items made by a third-party manufacturer and sold under a retailer’s brand name.

But when it comes to brand choice, the picture isn’t so clear. Sixty-three percent of shoppers say they’d still rather buy a brand-name item over a private label — even if it costs more.1

This gap between cost sensitivity and brand loyalty suggests that other factors may be driving consumer choices. Understanding the gap is key to building effective CPG media campaigns across the path to purchase, where the open internet allows brands to influence decision-making by showing up early and consistently.

The Trade Desk Intelligence and PA Consulting conducted a national survey of more than 3,000 grocery shoppers, which included an analysis aimed at uncovering the subconscious motivations behind shoppers’ brand selection.

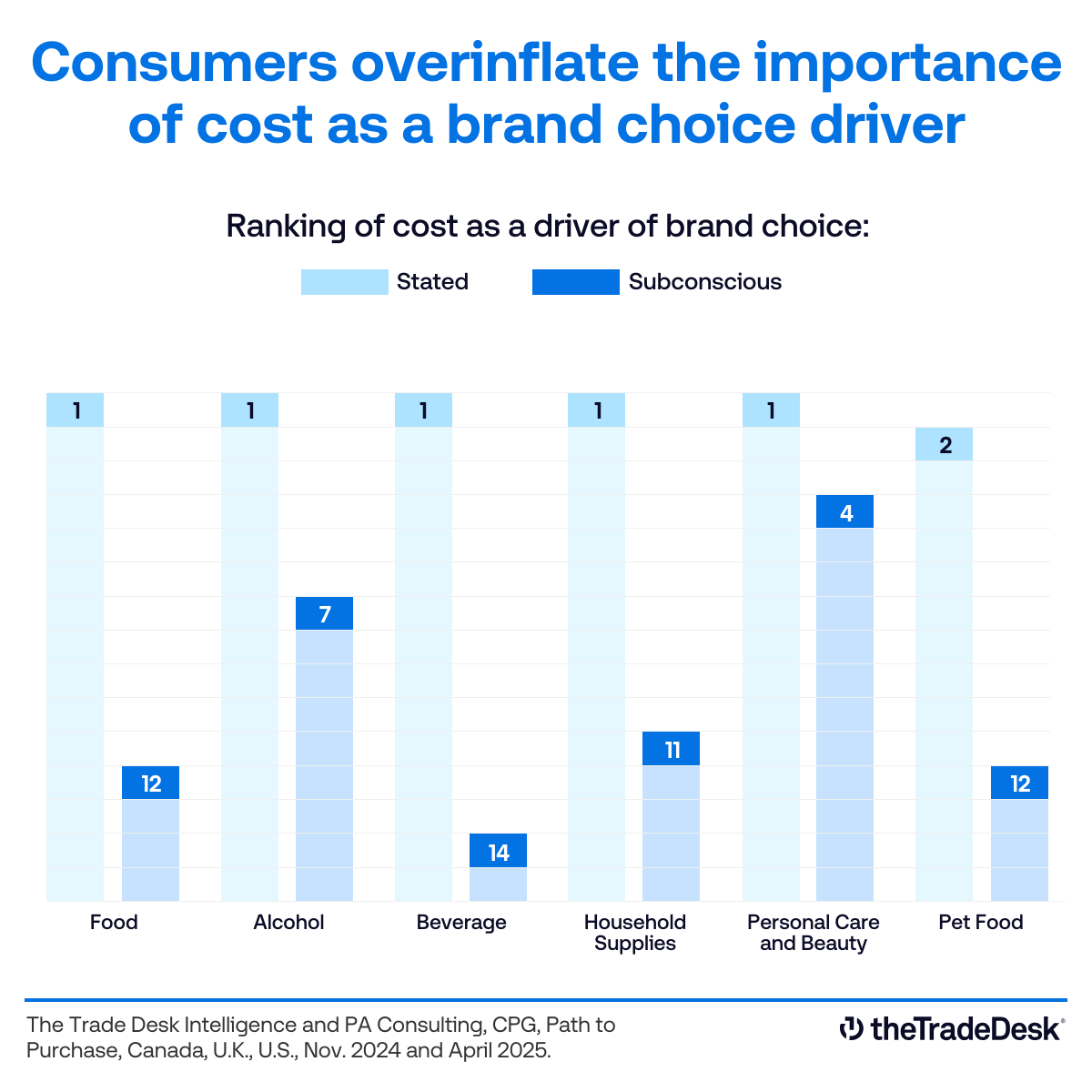

Respondents were given a set of attributes and asked to gauge their impact on purchase decisions. The results show that what people say motivates their choices doesn’t always align with why they ultimately choose a brand. For example, when asked about what matters most in general purchase decisions within a specific category, respondents ranked affordability the highest among 15 other attributes, including trust, humor, and familiarity.

Later in the analysis, respondents were asked to recall the last brand they purchased within a given category and then asked to determine how they would describe that brand by ranking the same 15 attributes.

Here, affordability fell much lower, implying that cost is subconsciously not as important a driver of brand choice as consumers might explicitly state. The data visual below illustrates how price subconsciously ranks much lower in actual purchase decisions than in stated preferences.

To better map the purchase journey, the second part of our study broke shopper behavior into three stages, Trigger → Consideration → Purchase, and looked at how marketing impacted these stages.

Across all six categories, we found that the consideration phase offers the strongest opportunity for influence. By the time shoppers reach the purchase stage, most have already made up their minds, making it harder for brands to shift behavior at the last moment.

When it comes to influence, the open internet beats walled gardens and traditional media at nearly every stage of the purchase journey. With 76% of shoppers’ digital time spent outside of social media,2 open internet environments (CTV, podcasts, online video, and premium display) emerge as critical spaces to reach and influence cost-conscious consumers before the point of sale.

Open internet ads are 28% more effective at driving product research than walled garden ads.1

CTV ads are 27% more persuasive than linear TV and 22% more persuasive than YouTube ads.1

Display/OLV ads are 28% more likely to boost buyer confidence than social media ads.1

While media behaviors vary slightly across categories, the broader pattern is clear: Reaching shoppers early and throughout their purchase journey is crucial for shaping decision-making.

Advertising in podcasts is the No. 1 trigger for food shoppers, offering an early opportunity to establish trust and relevance. Online video (OLV) extends that influence through the consideration phase.

Sources:

1. The Trade Desk Intelligence and PA Consulting, CPG, Path to Purchase, Canada, U.K., U.S., April 2025.

2. GWI, Canada, U.K., U.S., Q1-Q4 2024.

3. Alcohol, Personal Care/Beauty, Pet Food Path to Purchase: The Trade Desk Intelligence and PA Consulting CPG Path to Purchase, Canada, U.K., U.S., Nov. 2024.

4. Beverage, Food, HH Supplies PP: The Trade Desk Intelligence and PA Consulting, CPG Path to Purchase, Canada, U.K., U.S., April 2025.

Resources Our platform

Resources Our platform

Case Studies Omnichannel